Foundational to analysing any business starts with these questions:

How does the business make money;

What are the growth drivers;

Is the business model is Asset Heavy or Asset Light.

Today’s article focuses on the last point.

Asset Heavy businesses have a significant proportion of their total value tied up in fixed assets (plants, and equipment) and Net Working Capital (inventory and accounts receivable and payables).

The challenge with asset-heavy businesses is that carrying these on your balance sheet has a cost. Money isn’t free.

Every $1 tied up in your assets has an opportunity cost.

This is why investors look for “asset-light” businesses - there’s a high correlation between asset light businesses and ones that generate strong Free Cash flow.

Most businesses can’t escape investments in plant and machinery. Retailers expanding their footprint need to invest in new store fitouts. Manufacturers need to invest in new machinery to increase capacity.

What you can manage however is Working Capital.

Defining Working Capital

Working capital is the funding a business needs to meet its short term obligations. It’s the assets and liabilities that cycle through a business in less than 12 months.

Working Capital includes:

Receivables and Prepayments - Money you are owed by customers.

Inventory - The value of goods and work in progress held for future sale

Payables (inc. Accruals and Deferred Income) - Amounts invoiced by suppliers not yet paid. Sub categories are;

Accruals- costs incurred not yet invoiced by suppliers

Deferred/unearned revenue - cash received from customers for services not yet delivered. Common with SaaS on annual plans for example.

Net Working Capital (NWC) is derived by the formula:

NWC: Receivables + Inventory - Payables.

Most businesses have Positive Net Working Capital requirements, where

Receivables + Inventory > Payables.

There are some businesses that have Negative Net Working Capital requirements, where

Payables > Receivables + Inventory.

In this situation, working capital produces funding rather than needs it.

Overall, the goal for Managers is to get Net Working Capital as low as commercially possible.

By doing so, this frees up cash to reinvest back into growth, or pay distributions to shareholders.

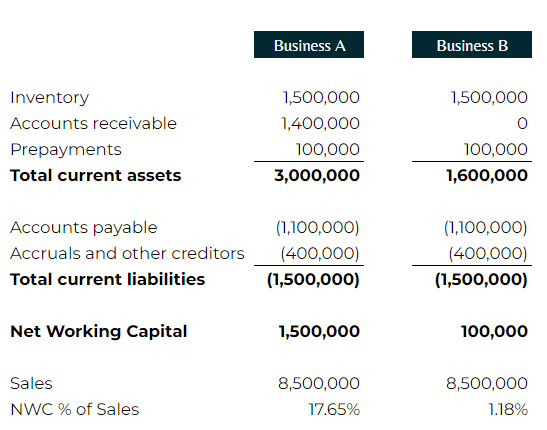

Let’s use an example to illustrate:

Business A & B, do the same thing, and are the same size - they both sell widgets.

Business A customers pay 60 days following shipment of the product

Business B customers pay 100% upon shipment of product.

The working capital position looks something like this for these two businesses:

Business A has $1,500,000 of positive net working capital.

Business B only has $100,000 of positive net working capital.

The difference between the two is $1,400,000.

Business A’s funding need is $1,400,000 higher than Business B.

This is permanent funding that Business A needs to find, that Business B does not.

The difference is huge.

A common issue I see with our clients at SBO Financial (our accounting firm) is that a lot of founders often focus on profit, but not Net Working Capital.

So how do you get everyone aligned?

We need a measure that combines the two.

Combining Profitability and Working Capital Management: Profit/WC

Swedish company Bergman & Beving is a publicly listed serial acquiror of building materials and industrial equipment businesses.

The company was founded in 1906 and today has over 20 companies with a $470M USD market cap.

Whilst most businesses focus on profitability, Bergman & Beving focus on cash flow - a common theme with serial acquirors. Working capital management is important to cash flow generation.

In 1981 the “Profit/WC metric” was introduced to help the portfolio company CEOs pay strict attention profit as well as working capital.

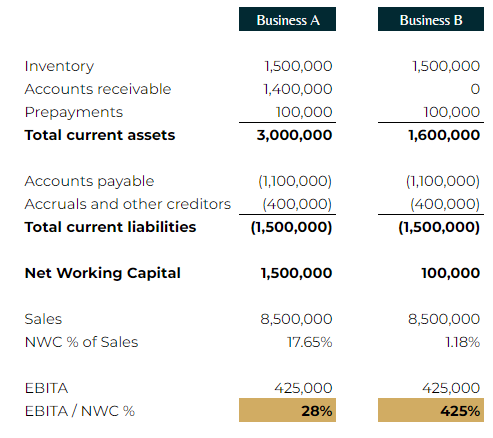

The formula is simple - you take EBITA (earnings before Interest, tax and amortisation) and divide that by Net Working Capital.

Profit/WC metric: EBITA / Net Working Capital

According to Bergman & Bevingsville, a business is considered self-financing when the return on working capital, calculated as EBITA / WC, is higher than 45%.

By achieving an EBITA/WC > 45%, the business can generate the necessary cash to cover taxes and make required investments in its existing business through capex, growth, and dividends.

The goal of being self-financed means that growth, whether organic or through acquisitions, will not dilute current shareholders through equity raises or rely heavily on debt. This highlights the importance of working capital efficiency in generating cash.

The idea of exceeding the 45% target was designed that free cash flow generated would cover:

one third tax,

one third dividends,

and one third growth (15% yearly growth measured over a business cycle, split between organic growth and acquisitions).

Applying the Profit/WC metric to our example above shows Business A doesn’t pass the threshold.

Business B on the other hand crushes it.

Despite having the same profitability, Business B generates $1,400,000 more cash than Business A. This is cash that could be used to reinvest in growth or paid as dividends.

Naturally, you want a Profit/WC ratio greater than 45%. It means more cash is being generated.

But how do managers take action with this information?

The Focus Model of > 45%

Bergman & Beving use an internal benchmark known as the "Focus Model." This model essentially serves as a benchmarking tool applied to all operating companies within the group, and their performance is evaluated accordingly.

The Focus Model for EBITA/WC levels is as follows:

Above 45%: Increase profits through revenue increases (organic and acquisitions)

Below 25%: Increase margins!

Between 25% and 45%: Increase margins and working capital turnover.

The Profit /WC ratio serves various purposes, such as assessing operating units, evaluating product performance, analysing markets and customers, and even assessing new business acquisitions.

Moreover, it is aggregated and measured at the holdco level. Ultimately, all employees receive incentives based on this profit ratio.

The overarching goal is for all employees to easily grasp and see the measurable impact on financial performance. This is a recurring theme among best-in-class companies, emphasizing straightforward financial objectives that genuinely make a difference, often tied to incentives.

The recurring lesson from these top performers is to avoid unnecessary complexity.

It's about establishing an internal language that resonates, especially for folks who may not be well-versed in financial jargon.

Simplicity is key.

Final thoughts on profit / working capital

Asset light businesses are necessary for serial acquirors because each business needs to generate high amounts of free cash flow to reinvest into organic growth and new acquisitions.

Without it, you’ll find yourself having to continually raise equity capital just to grow organically, let alone inorganically via acquisition.

This can result in destroying shareholder value, rather than growing it.

At Arbor Permanent Owners we use the EBITA/WC heuristic when we assess potential businesses to acquire. It’s a simple back of the envelope metric to ensure the business generates a high % of free cash flow.

The alternate method is to simply review the cash flow statement - however this report rarely exists in small business financial statements.

This is why it annoys me when I review information memorandums of businesses for sale that don’t contain balance sheets.

To the business brokers and corporate advisors reading this, please take note 😁.

About Arbor Permanent Owners

Arbor Permanent Owners is a Serial Acquirer holding company that acquires and invests in exceptional, private businesses, deliberately built for long-term success. Our goal is to be the long-term custodian and permanent home of Great Australian Small and Medium Enterprises (SMMEs).

We are actively looking for businesses with the following characteristics:

Business Model: B2B industrials: manufacturing and mission critical services

Business Size: $3 to $6 Million of EBITDA

Business Profile: Sticky B2B customer base

Business HQ: Australia

Whether you’re a business owner interested in working with us, or an intermediary with a deal to share, I’d love to hear from you. Please email us at [email protected]