Most companies are in the business of providing a service or product to the market. Landscapers providing landscaping services. Manufacturers making widgets for industry. Accountants providing tax services.

Serial acquirers don't produce any goods or services themselves. Rather, they are in the business of acquiring and owning smaller, cash flow positive businesses that serve the end customer.

They exist solely to buy businesses.

Serial acquirers are different from regular operating businesses that make strategic acquisitions to grow. They’re also different from investment firms like Private Equity.

The main difference being that serial acquirers are generally Principals, not Agents. This means they invest off their own balance sheet instead of managing other people’s money. Permanent capital is a critical ingredient of the serial acquirer business model.

This article by Ryan Krafft of investment firm Scott Management is regarded as the ‘seminal piece’ on serial acquirers.

I’ve done a bunch of research on the model and can say this is easily the best one we’ve come across. It does a fantastic job of defining and categorising serial acquirers, laying out why they’re attractive, and what one should broadly be looking for.

Here’s my summary.

How Serial Acquirers operate

The key characteristics of serial acquirers are:

The focus on acquiring small private niched businesses - frequently family-owned, with a solid financial record and organic growth, that often lack sufficient organic reinvestment opportunities to substantially absorb the cash flow they produce.

Inhouse M&A and diligence team - all diligence is conducted in house, following a repeatable streamlined process. This enables transactions to happen smoothly and quickly.

Upon entering a permanent capital home - these small niche businesses continue to produce strong cash flow. This cash flow is reinvested, generating higher returns on capital than their cost of capital for an extended period of time. Instead of distributing cash directly to shareholders, they retain much of it for future acquisitions.

Many successful acquisition-driven compounders operate with a decentralised organisational setup - customer relationships and daily business decisions are made at the subsidiary level, letting acquired companies preserve their culture and entrepreneurial independence.

HQ team is slim - and is focused on capital allocation, M&A and financial performance monitoring.

How are Serial Acquirers different from investment funds

Here’s a snapshot of how serial acquirers are different from traditional investment funds like private equity.

Defining and categorising serial acquirers

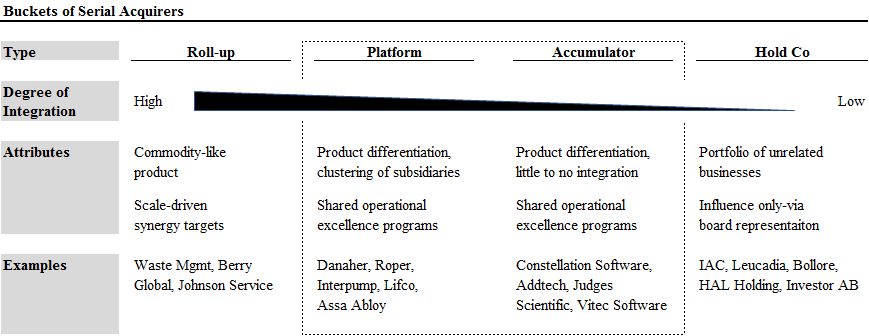

Serial acquirers can be bucketed into 4 forms: Roll-ups, Platforms, Accumulators and Hold-cos.

Source: Scott Management

Hold-Cos are at one end, holding largely unrelated businesses with no synergies.

Roll-ups are on the other end, focusing on one homogenous vertical with very high scale driven synergies (learn more about roll-ups here) podcast)

Platforms have a few specific platforms, inside which they are more tightly integrated and resemble “lite” roll-ups with some synergies, but mostly focus on improvement through high knowledge/skills transfer

Accumulators allocate capital broadly within many verticals in which they can acquire expertise but do not integrate or chase synergies.

There are some tell-tale signs of great serial acquirers, mainly around qualitative factors: structures, processes, culture and best practices.

Capital Allocation and cash flows

At it’s core, the key to a successful serial acquirer business model is the skill of the capital allocators at HQ.

The goal of capital allocation is to build long-term value per share. Being a great capital allocator can be compared to being a great investor; it is all about making the decisions that maximises shareholder value.

Great capital allocation is the use of cash that generates a return on invested capital (ROIC) higher than its cost of capital (WACC).

Cost of Capital → The cost of capital, or “WACC,” is the minimum rate of return that a company must exceed (i.e. the “hurdle rate”).

Return on Invested Capital (ROIC) → The ROIC measures the efficiency by which a company spends the capital contributions of equity shareholders and lenders to generate returns.

General Rule of Thumb

ROIC > Cost of Capital → Value Creation

ROIC < Cost of Capital → Value Destruction

The greater the spread between ROIC and WACC, the more value is created, and vice versa.

Acquisitions as a path to maintain ROIC

Many businesses, despite their past success, face ceilings in growth due for a number of reasons: local market saturation, regional constraints and other competitive pressures.

As a result, returns on capital will naturally diminish over time within the business.

The key feature of the serial acquirior business model is the ability to continue to reinvest capital over and above the hurdle rate by acquiring new businesses.

The result is unicorn companies that can grow for decades.

Final thoughts on Serial Acquirer business models

High quality serial acquirers make for wonderful investments as they can redeploy capital on your behalf for many, many years while simultaneously becoming more diversified and less risky. At scale, Cost of Capital reduces and more free cashflow is generated. The result is a capital compounding flywheel.

Scalability is a key criterion you need to evaluate when looking at a serial acquirer. The diminishing returns to M&A can only be delayed, not escaped, and scaling is a slow, deliberate process.

Investing in larger serial acquirers with a track record may provide a false sense of security. A rear-view mirror approach is often inappropriate because dis-economies of scale are real and what’s required to scale over the next 10 years probably isn’t like what was required to scale over the last 10 years. Simply put, smaller and more fragmented is generally better for all three: roll-ups, platforms and accumulators.

An accumulator that is thoughtfully scaling their M&A infrastructure and processes is extremely valuable.

About Arbor Permanent Owners

Arbor Permanent Owners is a Serial Acquirer holding company that acquires and invests in exceptional, private businesses, deliberately built for long-term success. Our goal is to be the long-term custodian and permanent home of Great Australian Small and Medium Enterprises (SMMEs).

We are actively looking for businesses with the following characteristics:

Business Model: B2B industrials: manufacturing and mission critical services

Business Size: $3 to $6 Million of EBITDA

Business Profile: Sticky B2B customer base

Business HQ: Australia

We are backed by a small group of co-investors, collectively on a mission to preserve the legacy of Great Australian SMMEs.

If you are a sophisticated investor and would like explore co-investment opportunities with us, please email us at [email protected]